Apple Inc.

Apple Inc. is an American technology company with headquarters in Cupertino, California, and was founded in 1976 by Steve Jobs, Steve Wozniak and Ronald Wayne. The company manufactures computers, smartphones, tablets and consumer electronics, while providing operating systems and application software. The corporation currently has approximately 93,000 employees and sells products in more than 115 countries worldwide. Currently Apple has a market capitalization of $ 751 billion and is the largest company in the world. Apple is currently listed in the S+P 500 and Nasdaq.

The corporation has presented the best quarterly result in the history of the company on January 27 this year and posted a net profit of $18 billion, which is also the best quarterly result in economic history at the same time. The record here was previously held the by the russian energy company Gazprom, which generated a quarterly earnings of $16.24 billion 4 years ago. This record and the never-ending hype surrounding the Apple Corporation is a reason to consider the company with a fundamental analysis more accurate and to work out how the stock is currently valued or how much potential the company still has in the future.

In this fundamental analysis, we will first take a look at the key financial ratios and work out how the company has developed in recent years. Furthermore, we will look at the industries in which Apple has been operating and at the same time we will consider the regions where the company generates most of its revenue. Finally, we will summarize with the help of a SWOT analysis the key points of this work and will give an outlook for the Apple stock.

Financial ratios:

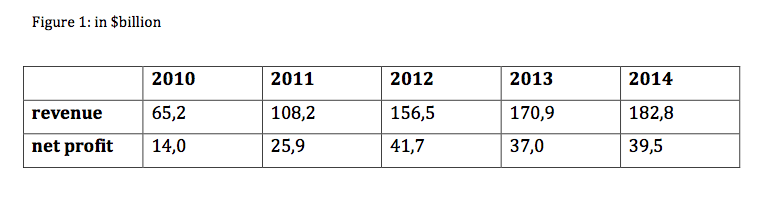

Apple increased its revenue by 180% over the past 5 years and generated $182 billion dollars in 2014 . Even more impressive is the sales trend for the last 10 years, because in 2004 Apple just generated $13.9 billion. This represents a sales growth of 1200% over the last 10 years.

However, over the last 2 years the net profit of Apple stagnated and the company recorded $39.5 billion profit in 2014 which is 5% less profit than 2012. The profit margin in recent years was a little lower because the company had a lot of cost with the production of new product updates and at the same time Apple brought out the iPad Mini which has a significant lower profit margin than any other Apple product.

The stagnation in net profit went to an end over the last quarter, because Apple could not only increase its sales by 30% compared to the previous year, but at the same time the company also increased it´s net profit from $13.07 billion to $18.02 billion, which represents an increase of 38%, respectively. This record result over the last quarter was mainly due to 2 reasons: firstly, sales in China increased by 70% and right now 21% of the total revenue is generated in China.

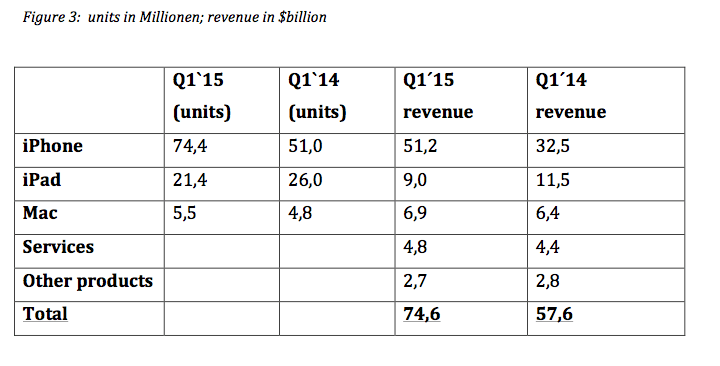

The second reason for the best quarter in the company’s history is the iPhone, from which Apple was able to sell over 74,4 million units over the last 3 months. This means Apple was able to sell around 574 iPhones per minute over the last quarter. Overall, Apple was able to increase it´s sales of the iPhone by 57% compared to the same quarter last year.

But sales of all other Apple products are stagnating at the moment e.g. the revenue of the iPad decreased 17% last quarter.

Apple currently has a price-earnings-ratio of 17.5 and this is below the average price-earnings ratio of Nasdaq 100 companies ( 22.5 ) and also from the S+P 500 ( 18.9 ), where Apple is listed in each case.

This shows that Apple is currently not overrated. Normally technology companies have anyway a slightly higher price-earnings-ratio than the market, which can be seen very clear at the Nasdaq 100. Even if Apple had a PER between 20-25, it would be in the normal range.

One of the most important financial key figures for long-term shareholders is the return on equity of a company, because it gives a clear indication of how profitable a company is. Finally, all investors will only invest if the company is consistently profitable.

Apple was able to generate a constant return on equity between 30-35% over the last 5 years, which is a really strong result, while the average return on equity in the S+P 500 was between 14-18 over the last 3 years. So right no Apple is able to earn a return on equity which is twice as high as the return on equity from the market. When an investor looks at the return on equity, at the same time he will also look at the equity ratio, to find out how the company leveraged it´s earnings. Apple currently has an equity ratio of 47%, which is extremely high for a company, which has a three digit total assets.

In the years before Apple could even displayed an equity ratio between 60% -67%. The reason for the reduction in this rate, is that Apple has issued a bond for the first time in 2013 and was making some long-term debt. Steve Jobs, who died at the end of 2011, was never a fan of making debt.

Currently, Apple has cash reserves of $178 billion with which the company could theoretically buy 480 out of 500 S+P 500 companies. The equity ratio and the current cash reserves give the company an extremely high financial stability. At the same time Apple is able to generate the double amount of return of equity in comparison to the market which is almost unique and because of this the Apple stock is one of the most traded stock worldwide.

Right now Apple has a dividend yield of 1.47%, which is below the average of the S+ P 500 which is 2%. The corporation just started to pay a dividend in 2012 and since then the company increased the dividend per quarter from $0,38 to $0,47.

This means that Apple pays an annual dividend of $1,88. If you consider that Apple this year is expected to generate earnings per share of about $9, that sounds like a very low payout ratio. However, Apple also started in 2013 a very large share buyback program and last year the company bought for $45 billion of its own shares . Such a buyback program is always very much appreciated by investors, as this leads to higher demand .

At the same time it decreases the number of shares that are in circulation, so that the earnings per share will increase if the company should generate the same net profit. This could also be observe very nice at Apple, since the earnings per share increased last year up to $6,49 (2013 : $ 5.72; 2012: $ 6.38 ), although we have already noted that the profits stagnated in recent years. The purchase of own shares also means that the company can distribute less dividend while the dividend per share will stay the same, because there are less shares outstanding. All those points will have a positive affect on the stock price.

Due to the current very high cash reserves the CEO , Tim Cook, said that the company does not want to unnecessarily hoard cash. And because of that statement a lot of analysts exspect a very large program for the shareholders. Currently there is the speculation in the market that Apple will announce a possible $150 billion program for the next 3 years in the near future. This is also realistic because Apple

has already bought for $45 billion it´s own shares over the last year and also paid about $ 11 billion of dividents.

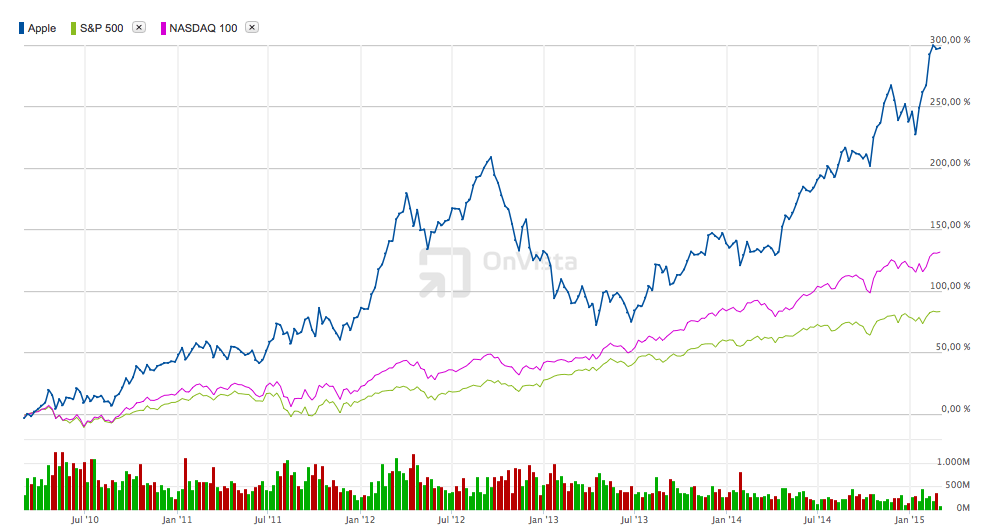

Because of the very strong return on equity ratio it is not a surprise, that the Apple stock was able to clearly outperform the S+P 500 over the last 5 years. During that time Apple share rose about 300% while the S+P 500 only moved up about 80%. The Nasdaq 100 rose about 130% during this time period. After the dead of Steve Jobs at the end of 2011, a lot of people already announced the end of Apple and the stock totally overreacted and made a very strong correction in 2012.

All together the financial ratios are looking very strong. The development of the revenue is really impressive and over the last quarter the company could end the short stagnation in net profits. Apple can stand up with a very high financial stability due to a strong equity ratio and very high cash reserves. During the year 2014 Apple generated a return of equity of 35% which is the double amount as the average ROE of the S+P 500.

Right now the dividend yield of 1,47% seems to be quit low, but at the same time Apple is doing a very large buy-back program.

But we have also noticed a weakness, because Apple is very much depending on the iPhone, because the sales of all other products are stagnating right now.

Industry analysis:

When we analyze the industries Apple is operating in, we have to take a special look at the smartphone industry, because we already saw that Apple is making most of it´s profit with the iPhone.

The smartphone industry was more or less created by the introduction of the iPhone in 2007. In 2014 more than 1,245 billion smartphones have been sold worldwide which is an increase of 28% in comparison to the previous year (2013: 970 million units). In 2014 Apple sold 169 million iPhones and during the last quarter the company was able to sell more smartphones than it´s main rival Samsung for the first time than 2011. Over the last 3 months Apple sold over 74,8 million iPhones while Samsung sold about 73 million smartphones.

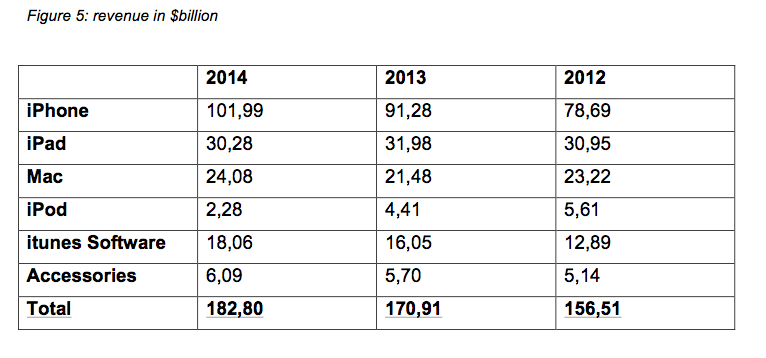

Especially the market in China rose significantly and also has more potential. Over the last quarter Apple made 69% of it´s revenue with the iPhone and there is a great chance that Apple can also improve this number because of the growing market in China.

The revenues of the iPad didn´t change at all over the last 3 years and the company was able to generate about $30 billion each year with the iPad over this time period. These numbers are quit weak, because the worldwide total sales of tablets increased about 60% over the last 3 years. Due to higher competition which are selling more and more cheaper tablets, Apple´s market share decreased from over 40% to just 29% in the tablet market over this time period.

Another important market is the computer market, which has been in a downtrend due to the tablet market. The worldwide computer sales decreased 14% over the last 3 years, but during the same time period Apple was able to hold it´s Mac´s sales constant. Right now the corporation has a market share of 6%.

If the computer market is going to continue it´s downtrend, it would be a quit good result for Apple if the company would hold it´s sales constant. We don´t expect any growth in the computer market over the next years.

When we look at the industries Apple is operating in, it is again clear to see that the iPhone is the biggest strength and weakness at the same time. The smartphone market is growing very strong and Apple is able to increase it´s sales each year and over the last 3 month the company was also able to sell more smartphones than it´s main rival Samsung. But Apple is very much depending on the iPhone, because the sales of all other products are stagnating. And in the long run it is always a problem for a company if it´s depending on just one product.

Apple has already noticed this weakness and is in the process of creating new products. On the 9th of March this year will be an event where Apple will introduce new products. We already now that Apple will come up with the Apple-Watch. Right now the smartwatch market is quit small and it will be very interesting to see how Apple fans will react to this new product.

Over the last weeks it was also confirmed that Apple is going to produce it´s own car until 2020 and will try to conquer a whole new industry. In recent years there were also a lot of speculation that Apple wants to sell it´s own television and this was also supposed to be the last project where Steve Jobs was working on.

The company will try to do anything to produce new products to offer a wide range of products, in order to reduce the dependence on the iPhone. And on the next Apple event all fans and investors will we looking forward to hear the legendary sentence:” And there is one more thing…”

Global economy:

The most important market for Apple is the USA, where the company was able to generate 36% of it´s revenue in 2014. Currently the economic situation in the US is quit good and can convince in contrast to Europe or Asia. Right now the US economy is growing very strong due to the very good labor market conditions. The US is depending very much on the labor market because it´s primarily a consumer society and because of that it is very important that a lot of Americans have a constant income.

This is also very important for Apple, because the company is producing luxury products and only in a growing economy a lot of people will be able to buy these products.

In Europe the company made 22% of it´s revenue last year. Right now the Eurozone has a lot of problems and the economy has still not recovered from the last recession and the unemployment rate is over 10% At the same time Greece is also a large uncertainty.

Therefore and because of the risk of deflation the European Central Bank decided to start with a large quantitative easing program whereby the EZB will buy private and public bonds for more than 1.000 billion euro to bring the European economy back on track. But this is no guarantee that the European economy will get stronger.

A big growth driver for Apple is currently China. As we already mentioned over the last quarter the revenue in China increased over 70% and there is still a lot of potential. In 2014 the company generated 16% of it´s total revenue in China. But a the same time the Chinese economy is growing as bad as over the last 25 years and China is not only an important market for Apple but also the most important factor for the worldwide economy.

The situation on the stock market is currently not so easy to analyze because on the one hand we have some worldwide economy problems but on the other hand a lot of stock indices are at their all time high and a correction is more likely.

However this correction might get push back at some point in the future due to the ECB QE-Program. If the stock market would do a correction, almost every stock would also decrease. That´s why it is important to find out how much a stock is depending on the market movements.

A good financial ratio to find out this is the beta-factor, which indicates the systematic risk of a stock. This ratio shows how volatile a certain stock behaves in comparison to the overall market. If the market makes a movement of 20% and one certain stock also moves 20%, this stock has a beta-factor of 1. If this stock would have made a 30% movement, the beta-factor would be 1,5.

Over the last 12 month Apple had an beta of 0,96 which is quit low for a technology company.

Conclusion:

At the end we will now summarize the most important facts of this analysis with the help of a SWOT-Analysis.

The analysis of Apple shows a very positive picture of Apple. In the case of financial ratios there is probably no company in the world that can compete with Apple. Last year Apple achieved a ROE of 35%, which is twice as high as the average return on equity of the market. The company also has a very high equity ratio and cash reserves, which gives the corporation a very strong financial stability. The high cash reserves ensure that the company can completely distribute it´s total net profit to their shareholders. And that is also the reason why the market is expecting a possible $150 billion program from Apple where the company will not only pay dividends but will also continue with it´s buy back program.

Our analysis clearly shows that the iPhone is currently the biggest strength and weakness of the company. This product is right now bringing the company more and more money each year. Especially China gave the iPhone sales a huge boost. But this means also a great dependency on one product. That´s why Apple is working on developing new products and it will be very interesting to see how good the new iWatch will do.

The high cash reserves also allow able to enter new industries like the automobile industry. Right now there are already some rumors about a possible cooperation between Apple and BMW and Tesla.

Bottom line is that Apple is currently well positioned and is about to open up new industries. And at the same time the market in China has a lot more potential in the future.

Medium- and long-term outlook:

The stock is currently near it´s all time high and this is not the best time to enter any stock. However an investor can already take advantage of some minor corrections to buy the stock. Should the market make a stronger corrections a long-term investor should definitely use this correction to take position in the Apple stock.

But it can also happen that the stock will not do any bigger correction since the current price-earnings ratio is quit low from Apple in contrast to the market (S+P 500; Nasdaq 100).